An IRS Revenue Officer is a field agent who visits taxpayers to collect unpaid taxes and secure unfiled returns. They conduct investigations of individuals and businesses, create payment plans, and file liens or issue tax levies if necessary. The IRS typically assigns a revenue officer when a taxpayer owes substantial back taxes, ignores multiple notices, or defaults on the payment agreement. If a revenue officer has contacted you, it means you have outstanding tax liabilities with the IRS.

At Victory Tax Lawyers, our seasoned tax professionals can help clients facing an IRS Revenue Officer's investigation. Schedule a free tax attorney consultation today.

This guide explains what IRS Revenue Officers do, why they are assigned to cases, and how a tax attorney can help protect your rights.

What Are the Key Responsibilities of an IRS Revenue Officer?

Revenue Officers are employees of the Internal Revenue Service (IRS) responsible for field collections. Unlike revenue agents or automated collection system representatives, revenue officers work directly with taxpayers to resolve unpaid federal tax liabilities and may visit homes or businesses as part of their investigations.

Their primary role is to gather financial information and determine a taxpayer's ability to pay. Revenue Officers review tax returns, bank statements, financial records, and third-party information to evaluate collection options and identify assets available to satisfy tax debts. They also negotiate installment agreements, partial-payment arrangements, and currently not collectible status when a taxpayer's financial circumstances support relief.

When voluntary compliance fails, Revenue Officers can take enforcement action. They may file a Notice of Federal Tax Lien, issue bank levies and wage garnishments, and pursue other collection measures authorized by law. In business tax cases, they can also investigate and assess the Trust Fund Recovery Penalty against individuals responsible for unpaid payroll taxes under IRC § 6672.

Revenue Officers operate under the Internal Revenue Code, Treasury Regulations, and the Internal Revenue Manual. As civil collection employees, they are not criminal investigators, but they have broad authority to request records, conduct interviews, and require taxpayers to submit financial disclosure forms. Since Revenue Officers often remain assigned to a case until it is resolved, taxpayers generally have more options available when they address the matter early.

What Skills and Qualifications Are Required to Become an IRS Revenue Officer?

A bachelor's degree is required for Revenue Officers, typically in accounting, business administration, finance, or a related field. Candidates with a certified public accountant credential or equivalent accounting experience also qualify under the IRS recruitment pathway. Tax specialists with prior work at the state level often enter through this door.

Candidates can qualify for IRS Revenue Officer positions through education or specialized experience. Specialized experience includes prior work in tax examination, collections, or financial analysis at federal, state, or private-sector employers.

Strong investigative, analytical, and interpersonal skills are also valued. Officers need working knowledge of the Internal Revenue Code, the civil laws governing secured debts, and the procedural rules in the Internal Revenue Manual. Negotiation skills matter as much as technical knowledge, because most cases close at the bargaining table rather than at a levy.

IRS Revenue Officers must pass a background check and undergo fingerprinting before hire. They must also hold a valid state driver's license, because the position requires field travel across an assigned territory and the officer is responsible for visiting taxpayer locations directly.

Training is structured. The IRS administers classroom instruction on the IRC and the Internal Revenue Manual, supervised on-the-job training in field collection, and ongoing technical training as procedures change. Some new-employee orientation draws on Federal Law Enforcement Training Center infrastructure used across federal civilian positions. The table below summarizes the qualifications profile in one view.

| Category | Requirements and Qualifications |

|---|---|

| Required Education | Bachelor's degree from an accredited college or university. Degrees in accounting, business administration, finance, economics, or a related field are preferred. A certified public accountant (CPA) credential or equivalent accounting experience may also satisfy qualification requirements. |

| Preferred Experience | Experience in tax examination, tax collection, financial analysis, accounting, auditing, or comparable federal employment. Prior accounting or tax-related experience can strengthen a candidate's application. |

| Essential Skills | Strong investigative and analytical abilities, effective communication and negotiation skills, knowledge of the Internal Revenue Code, and familiarity with civil collection laws governing secured debts and tax enforcement. |

| Training Provided | IRS-administered training covering the Internal Revenue Code, Internal Revenue Manual, collection procedures, taxpayer rights, and field investigations. New Revenue Officers also receive supervised on-the-job training and ongoing technical education as tax laws and IRS procedures evolve. |

According to IRS workforce data, the agency employed approximately 3,036 Revenue Officers in fiscal year 2024, compared to 2,820 in fiscal year 2023. These employees are responsible for collecting delinquent taxes and securing unfiled returns throughout the country. The increase reflects the IRS's broader effort to strengthen tax compliance and enforcement operations.

What Is the Work Environment, and What Challenges Do IRS Revenue Officers Face?

Revenue Officers spend significant time outside the office, and visits to homes and businesses are standard. A taxpayer who finds a Revenue Officer's business card on the door has been visited and missed; the card invites a call back, and silence is read as non-cooperation. IRS Revenue Officers are unarmed civil employees focused on collection. They are not the same as IRS Criminal Investigation special agents, who are armed, sworn federal law enforcement officers and handle criminal tax cases.

Taxpayers often panic at a Revenue Officer visit because they confuse the two, and that panic drives bad decisions about what to say and what to hand over. Officers work cases involving uncooperative or hostile taxpayers. They operate within legal constraints under the Taxpayer Bill of Rights and Collection Due Process protections, confronting families and small businesses during financial hardship.

Safety protocols exist for a reasonable reason. Officers travel in pairs in certain situations, coordinate with local revenue offices on field assignments, and follow IRS-established de-escalation procedures when a taxpayer becomes uncooperative. A measured tone from the taxpayer side opens more doors than confrontation.

The reasonable response to a Revenue Officer visit is to seek representation early. The mistake we see most often is the taxpayer who tries to handle the first three contacts alone and only calls counsel after a levy is placed on their payroll. Revenue Officers respond differently to a taxpayer represented by an experienced attorney than to a self-represented taxpayer, and the conversation shifts from collection demands to procedural resolution.

"In our experience, taxpayers often make their biggest mistakes during the first interaction with a Revenue Officer. Statements made early in the investigation can affect collection strategy, financial disclosure requirements, and enforcement decisions later in the case," says Parham Khorsandi. "Taking time to understand your rights before responding is often one of the most important steps you can take."

Speak with our team if a Revenue Officer has visited your home or business. We handle direct IRS contact from intake forward under Form 2848, and we coordinate every officer conversation, document request, and financial disclosure on your behalf.

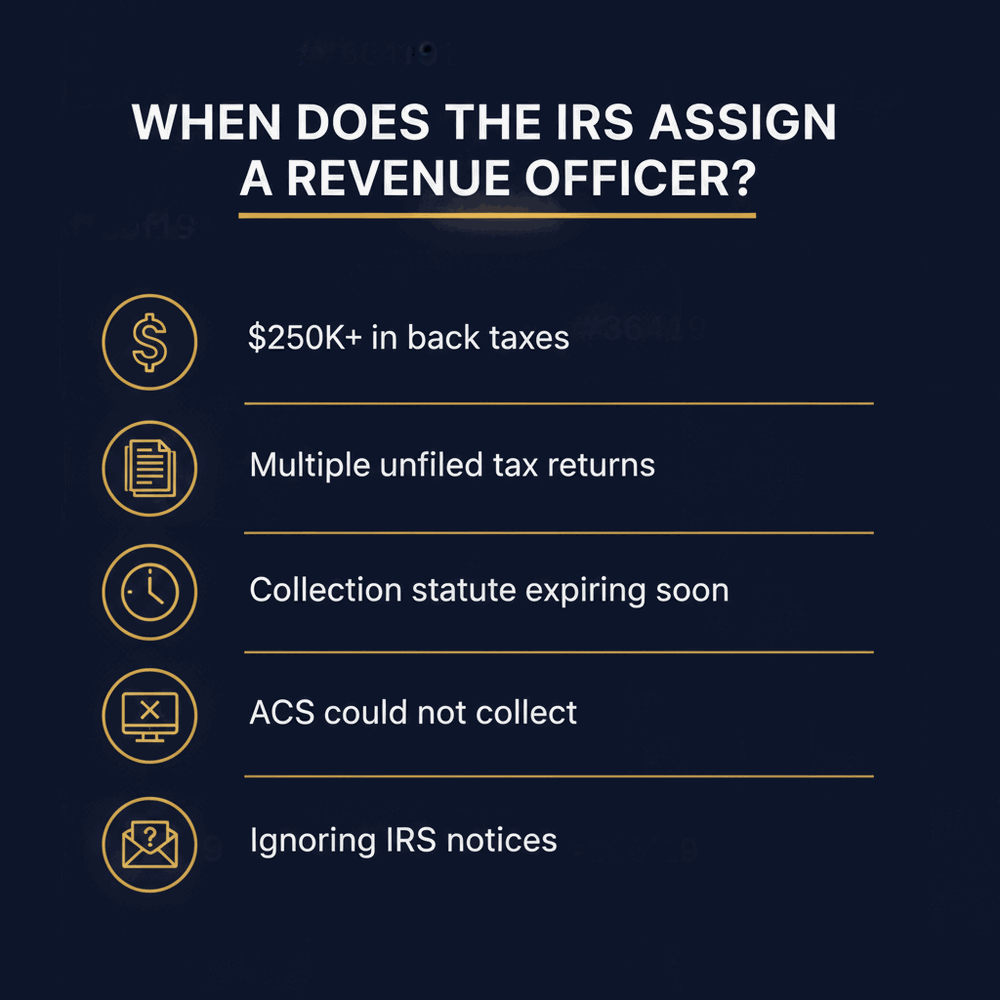

When Does the IRS Assign a Revenue Officer?

Revenue officers are often a last resort for the IRS after the agency has already sent a taxpayer multiple notices or even taken further action. When your case is assigned to a revenue officer, it means the IRS considers your situation serious enough to require direct attention and stronger collection efforts.

Revenue Officers are generally assigned to high-priority cases, often involving back taxes exceeding $250,000. However, balance alone is not the only factor. They may also be assigned if a taxpayer has multiple unfiled or delinquent returns, even when the total debt is smaller.

Revenue Officers may also be assigned if the statute of limitations on collections is about to expire and the IRS needs someone to pursue the balance before the deadline passes. Finally, they may be assigned to you if the IRS believes you've been avoiding making payments. Regardless of the reason, once they are on your case, it can be stressful to get them removed.

If you're contacted by an IRS revenue officer, it is important not to panic or make any hasty decisions. Your best course of action is to get in touch with a tax attorney as soon as possible. Once you've made the request, the officer must pause the interview or investigation until your legal counsel is present.

Unlike most IRS communications, which are typically mailed as letters or notices, interactions with Revenue Officers are usually more immediate and personal. In many cases, a Revenue Officer's first interaction with a taxpayer is an in-person visit. Although they may also reach out by phone, face-to-face communication is usually preferred.

Even if your property has a No Trespassing sign, IRS Revenue Officers are legally allowed to access publicly accessible areas such as a front porch, driveway, or business lobby. However, if you request that they leave, they must comply. If a Revenue Officer cannot reach you directly, the officer may contact family members, neighbors, employers, or others who can provide information about your whereabouts or financial situation.

Can a Revenue Officer Be Removed From Your Case?

In most cases, taxpayers cannot simply request that a Revenue Officer be removed from their case. Revenue Officers are assigned by the IRS based on factors such as the amount owed, unfiled tax returns, compliance issues, or the complexity of the case. However, the level of involvement may decrease once the taxpayer becomes compliant and a resolution is in place.

For example, after required returns are filed and a payment arrangement is approved, some cases may be transferred back to automated collection systems or monitored with less direct oversight. The best way to reduce Revenue Officer involvement is not to avoid contact, but to address the underlying tax issues promptly and work toward a sustainable resolution.

How a Revenue Officer Case Typically Develops

A business owner contacted our firm after receiving several IRS notices regarding unpaid payroll taxes totaling approximately $185,000. After months of missed payments and unfiled employment tax returns, the IRS assigned a Revenue Officer to the case.

The Revenue Officer requested financial records, scheduled interviews, and began evaluating whether a Trust Fund Recovery Penalty investigation was appropriate. Rather than communicating directly with the officer, the taxpayer retained legal representation and executed Form 2848, authorizing counsel to act on their behalf.

Our team worked with the Revenue Officer to bring the business into compliance with filing requirements, submit financial disclosures, and negotiate a collection resolution. As a result, the taxpayer avoided immediate levy action and secured a structured resolution that allowed the business to continue operating while addressing its tax obligations. Every case is different, but this example illustrates how quickly an unpaid tax matter can escalate once a Revenue Officer becomes involved.

What Are Your Rights When Dealing With a Revenue Officer?

Before meeting with a Revenue Officer, organize financial records in advance and avoid providing documents that were not specifically requested. Keep copies of everything submitted and maintain a written record of all communications. These simple steps can help prevent misunderstandings and facilitate more productive future negotiations. When dealing with a Revenue Officer, you still have your rights as an individual and can make certain requests. Here are some important actions to take to protect yourself:

1. Request To See Their Official Identification

If a Revenue Officer visits you, ask to see their official IRS identification card or badge. All IRS employees are required to carry one. If they cannot provide it, you are not obligated to continue the conversation.

2. You Can Demand Their Manager's Contact Details

You may also request the contact details of the Revenue Officer's manager, especially if you believe the officer is acting improperly. Every revenue officer reports to a manager, and they are required to give you that manager's contact information if you request it. You can also request a call from the manager yourself.

3. You Have The Right To Legal Representation

When a Revenue Officer contacts you, they must provide Publication 1, an official IRS document that details your rights as a taxpayer. This publication explains examination, appeal, collection, and refund processes, and it emphasizes your right to fair, courteous, and professional treatment. If you ever feel that your rights, as described in the publication, are being overlooked or violated, you have the right to express your concerns.

4. You Can Record the Interview

Few taxpayers realize that they are legally allowed to record an in-person interview with an IRS Revenue Officer. In fact, during any meeting with an IRS employee, you have the right to take notes or even request that someone tag along with you. Just remember to inform them about your intentions and reasons at least ten days before the scheduled meeting.

What Is the Difference Between an IRS Revenue Officer and a Revenue Agent?

Many people confuse a Revenue Officer and a Revenue Agent. However, these roles are distinct within the IRS. Revenue Officers focus on collecting delinquent taxes and securing unfiled returns, while Revenue Agents handle tax audits to verify the accuracy of reported income, deductions, and credits.

IRS Revenue Agents typically have an accounting background and focus on auditing taxpayers to determine the correct tax liability. If they identify underpaid taxes, this may result in an additional assessment on the extra amount owed. Once a balance remains unpaid, the case is referred to a Revenue Officer for collection.

Unlike Revenue Officers, Revenue Agents cannot garnish wages or seize assets. In contrast, ROs have significantly more authority to enforce tax collection. If you are facing an IRS audit, our experienced tax attorneys can provide comprehensive assistance. Schedule a consultation today to learn more about our IRS audit representation services.

How Can You Confirm That an IRS Revenue Officer Is Legitimate?

With IRS-related scams on the rise, it is crucial to verify the identity of a Revenue Officer before interacting with them. Here are several ways taxpayers can confirm that an IRS Revenue Officer visiting them is legitimate.

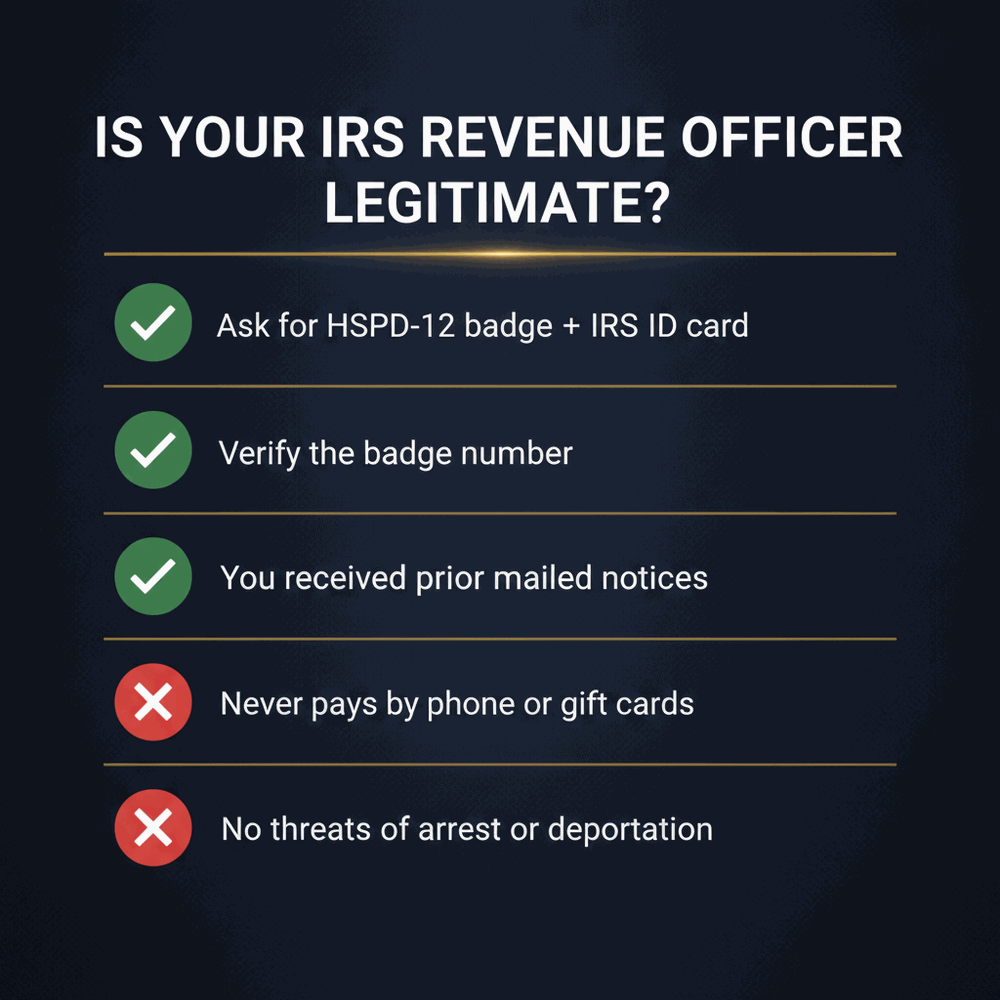

You should have received multiple IRS notices by mail before a Revenue Officer ever visits you. These letters typically explain your tax debt, outline collection efforts, and provide instructions for resolving the balance. If someone claiming to be an IRS Revenue Officer visits you without any prior IRS correspondence, proceed with caution and verify their identity.

When meeting with a Revenue Officer, ask to see their official identification. Every IRS Revenue Officer carries two forms of ID: an HSPD-12 badge (a federal government photo identification card) and an IRS-issued employee identification card. If the individual cannot provide these credentials, or if you have any doubts about their legitimacy, contact your local IRS office to verify their identity.

You can also verify the officer's badge number. Each IRS employee has a unique identification number, often referred to as a badge number. Contacting the IRS directly can help confirm that the individual is an authorized employee and that the badge number is valid.

Remain alert for suspicious behavior. The IRS generally communicates through mailed notices, and Revenue Officers are typically assigned only after previous collection efforts have been made. If you receive an unexpected phone call from someone claiming to be with the IRS, especially if you have not received any prior correspondence, hang up and contact the IRS using an official phone number.

It is also important to recognize common signs of tax scams. Revenue Officers do not carry weapons and do not have the authority to make arrests. Any threats of immediate arrest, deportation, or other criminal consequences are strong indicators of fraud. Likewise, the IRS never demands payment through gift cards, prepaid debit cards, wire transfers, or similar methods.

Neither the IRS nor a Revenue Officer will ask you to make a payment over the telephone. If you choose to pay by check, it should be made payable only to the U.S. Treasury and never to an individual or private entity. If you are unsure whether a Revenue Officer is legitimate or feel uncomfortable handling the situation on your own, consider seeking assistance from a qualified tax professional.

Revenue Officer Assignment Vs. Automated Collections

The IRS typically assigns most unpaid tax accounts to the Automated Collection System (ACS) before involving a Revenue Officer. ACS is designed to handle routine collection matters through automated notices and remote IRS representatives, making it an efficient option for lower-priority cases.

ACS generally manages accounts involving tax debts under $100,000, particularly when there are no complex issues such as delinquent tax returns, business ownership, corporations, non-profit organizations, or signs of noncompliance. ACS representatives can answer questions about your balance, payment options, applicable tax code provisions, and related regulations, but they do not conduct field visits or extensive investigations.

In most cases, ACS is used when a taxpayer owes less than $100,000, has no significant delinquent tax returns, and has not been flagged for prior enforcement actions, tax audits, or potential tax evasion. When these factors are absent, the IRS can often resolve the matter through notices, phone calls, and payment arrangements without assigning the account to a local field officer.

If ACS cannot resolve the issue, the IRS may assign the account to a Revenue Officer. Revenue Officers handle more complex cases that require direct contact with taxpayers, businesses, corporations, or non-profit organizations. They may gather evidence, investigate financial circumstances, review compliance issues, and take additional enforcement steps when necessary.

Since their career is focused on tax collection and compliance, Revenue Officers are typically assigned when the IRS believes more direct involvement is needed to resolve the case. In some situations, unresolved disputes may ultimately progress to administrative appeals or court proceedings, making it important to have a clear understanding of your rights and obligations under the tax laws and related regulations.

Is a Revenue Officer Assignment Always Bad?

A Revenue Officer assignment often means the IRS considers your case more serious than accounts handled through the Automated Collection System. However, there can be advantages to working with a dedicated Revenue Officer. Unlike ACS representatives, who generally have limited authority and rotate frequently, Revenue Officers remain assigned to a case and can evaluate financial circumstances in greater detail. In some situations, this can create opportunities for more customized resolutions.

The trade-off is that Revenue Officers also possess greater enforcement authority. While ACS generally relies on notices and phone calls, Revenue Officers can investigate assets, request extensive financial information, and pursue collection actions more aggressively when taxpayers fail to cooperate. Whether a Revenue Officer assignment ultimately helps or hurts depends largely on how quickly the taxpayer engages and whether a viable resolution strategy is presented.

The VICTORY Revenue Officer Response Framework

A Revenue Officer assignment does not mean you have lost your options, but it does require immediate attention. Taking the right steps early can help protect your rights, preserve available resolution options, and reduce the risk of aggressive IRS collection actions. Our VICTORY Framework outlines a practical approach for responding when a Revenue Officer contacts you.

V – Verify Identity: Confirm the officer's credentials, badge number, and IRS identification.

I – Identify Deadlines: Determine whether the IRS has imposed deadlines for financial disclosures, tax return filing, or payment arrangements.

C – Collect Records: Gather tax returns, bank statements, payroll records, and supporting financial documentation.

T – Transfer Communications: Consider appointing a representative through Form 2848 so communications can be directed through counsel.

O – Organize Resolution Options: Evaluate available solutions such as installment agreements, currently not collectible status, penalty relief, or an offer in compromise.

R – Respond Promptly: Failure to respond often increases enforcement risk and limits available resolution options.

Y – Yield a Long-Term Compliance Plan: The ultimate objective is not only to resolve current liabilities but also to maintain future compliance to prevent additional collection actions.

Although Revenue Officers have significant collection authority, their objective is not simply to levy assets whenever possible. IRS policy generally encourages voluntary compliance and negotiated resolutions when taxpayers cooperate and provide accurate financial information. In many cases, proactive communication can prevent more aggressive collection actions.

Need Help With an IRS Investigation?

Many online articles describe what an IRS Revenue Officer does. This guide goes further by explaining how Revenue Officer cases actually progress, what triggers assignment, how enforcement decisions are made, what rights taxpayers retain during the investigation process, and what practical steps can reduce collection risk.

With over $72 million saved for clients since 2017, Victory Tax Lawyers, a Los Angeles-based tax firm, delivers experienced legal help you can count on to get real IRS solutions. Get the help you deserve. Contact us for a free consultation today!

Frequently Asked Questions

This section provides answers to frequently asked questions about the role of an IRS Revenue Officer.

What Is the Role of an IRS Revenue Officer?

The role is the civil collection of unpaid federal taxes through field visits, payment plan negotiations, and lien and levy actions. Revenue Officers also assess the Trust Fund Recovery Penalty under IRC § 6672 when a business has not remitted employment taxes.

What Skills Do IRS Revenue Officers Need?

Officers need strong investigative analysis, interpersonal communication, and working knowledge of the Internal Revenue Code and civil collection law. They also need the ability to read complex financial matters quickly and apply that reading to a defensible collection decision.

How Much Do IRS Revenue Officers Earn?

Revenue Officers are paid on the federal General Schedule, typically across the GS-7 through GS-13 range depending on grade and locality. Specific pay tracks GS grade plus geographic locality pay, which the Office of Personnel Management adjusts annually.

What Is the Training for an IRS Revenue Officer?

IRS revenue officers must undergo extensive training in tax law, business law, investigative techniques, and collection procedures. The program includes classroom instruction and on-the-job experience to ensure officers are prepared to handle complex tax situations.

Why Would an IRS Revenue Officer Contact You?

An IRS revenue officer would contact you if you have delinquent taxes, unfiled tax returns, or if you have ignored all attempts by the IRS to resolve the issue. Their responsibility is to collect taxes owed and ensure future tax filing requirements.

What Powers Do IRS Revenue Officers Have?

IRS revenue officers have the authority to file federal tax liens against the properties of an individual who defaults on tax payments. They are permitted to request financial information from third parties such as employers or banks, and can make an unannounced visit to an individual. They are vested with the power to collect unpaid taxes and enforce compliance, either through levies or asset seizure.

What to Do if an IRS Revenue Officer Contacts You?

If an IRS officer contacts you and you have an in-person meeting scheduled, you should request identification. They are expected to have a pocket commission and an HSPD-12 card, both of which should display their photo and serial number for official identification. After verifying the officer's identity, they may review your documents and discuss your tax situation. You must cooperate with them and provide them with the necessary information they need.

How Does a Visit from a Revenue Officer Differ From Other IRS Contacts?

A revenue officer's visit differs from other IRS contacts because it is typically an in-person meeting rather than merely letters, phone calls, or notices sent by mail. Unlike these other forms of contact, the officer can request bank account statements, set deadlines, establish an installment agreement, and initiate enforcement actions.

How Much Tax Debt Triggers an IRS Revenue Officer Assignment?

No fixed tax debt triggers an IRS revenue officer assignment. Cases are assigned to these officers only when the IRS considers the tax liability to be significant, long overdue, or high-risk. In situations where the IRS's Automated Collection System (ACS) fails to collect taxes, a revenue officer may be assigned.

Is It Possible to Negotiate Directly With a Revenue Officer?

Yes, you can negotiate directly with a revenue officer. It is part of their job performance in resolving unpaid taxes through payment plans, extensions, or other collection alternatives. Many taxpayers choose to involve a tax professional, such as a CPA, tax attorney, or Enrolled Agent (EA).

Legal Disclaimer: This content is provided for informational purposes only and does not constitute legal or tax advice. Reading this article does not create an attorney-client relationship. Tax situations vary, and you should consult a qualified tax attorney or tax professional regarding your specific circumstances before taking action.