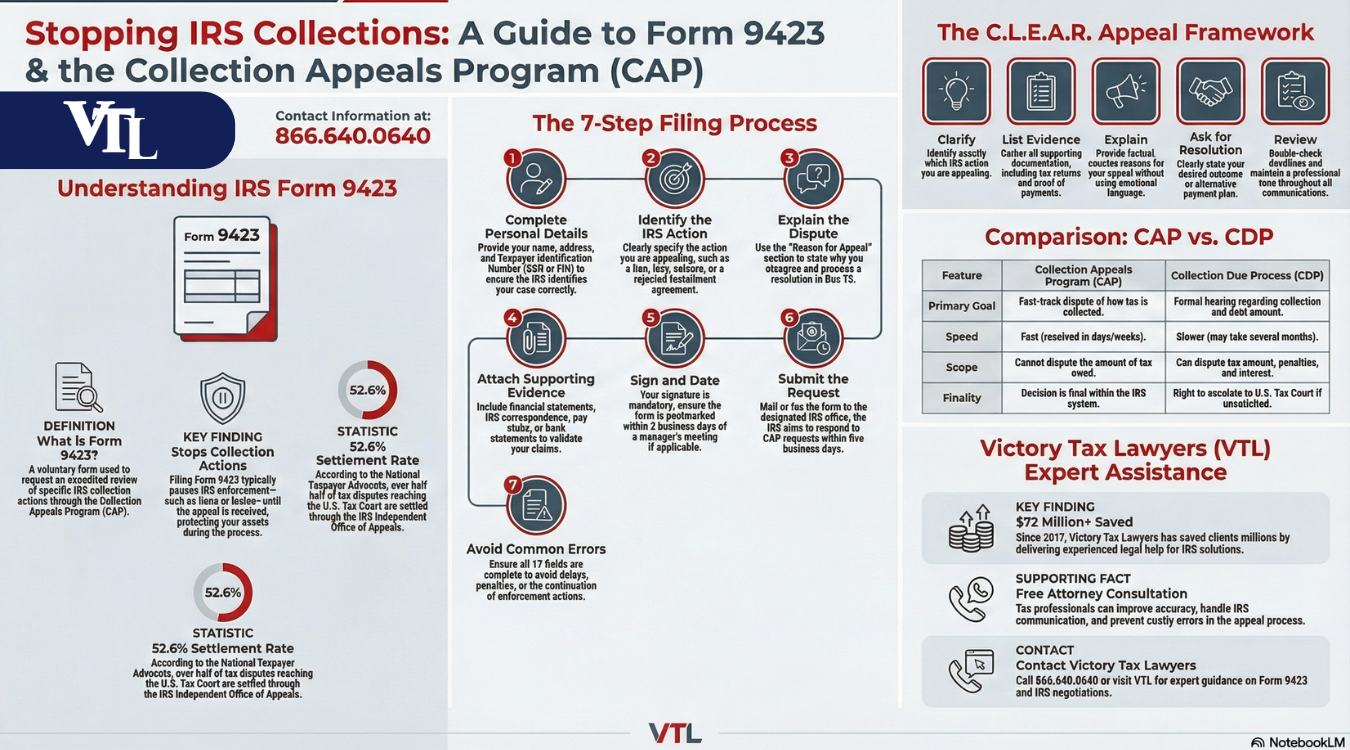

The Collection Appeal Request Form 9423 allows taxpayers to challenge a proposed collection action by the IRS and request a CAP hearing before further collection action occurs. You file the tax form with your taxpayer signature to dispute unpaid taxes or other IRS decisions that the agency believes justify enforcement. The IRS’s independent office reviews the appeal according to internal revenue code sections and the tax code, potentially preventing economic harm. Filing correctly can stop the IRS from acting, let an IRS supervisor review the case, or ensure the IRS terminates inappropriate collection measures, resolving your tax problem.

At Victory Tax Lawyers, our seasoned tax professionals can help with the filing of IRS Form 9423. Schedule a free tax attorney consultation today.

In this guide, we’ll explain what Form 9423 is, how the Collection Appeals Program works, and when it’s worth filing.

What Is IRS Form 9423 and How Do You Use It to Challenge IRS Collection Actions?

Taxpayers can formally contest IRS collection actions, such as liens, levies, property seizures, or denied installment agreement requests, by submitting IRS Form 9423. This is also referred to as the Form 9423 collection appeal. To contest the IRS’s suggested actions, any taxpayer with tax debt that the IRS deems worthy of enforcement may submit this 9423 collection appeal request.

The form needs to be filled out in accordance with the guidelines and sent to the relevant IRS office or via the IRS website. The IRS independent office reviews these appeals to ensure fairness and compliance with internal revenue code sections and the broader tax code, offering an opportunity for a tax dispute to be resolved before further collection action occurs.

According to the National Taxpayer Advocate, 52.6% of tax disputes that reach the U.S. Tax Court are settled through the IRS Independent Office of Appeals rather than decided by a judge. This demonstrates the effectiveness of a well-prepared appeal.

Filing at the right time can temporarily pause enforcement and allow for a CAP hearing or review by an IRS supervisor. Misunderstandings are common, such as assuming the form can stop all collection permanently or that any IRS request for payment must be accepted without appeal. Failure to file properly or on time can escalate the IRS’s actions, creating unnecessary economic harm or additional penalties.

IRS Form 9423 vs. Related IRS Forms

| Form Name | Purpose | Filing Requirement | Common Use Cases | Penalties for Non-Compliance |

|---|---|---|---|---|

| Form 9423 — Collection Appeal Request | Requests an appeal of an IRS collection action (e.g., levy, lien, seizure) through the Collection Appeals Program (CAP) | Filed when you disagree with a specific collection action and want expedited review | Challenging bank levies, wage garnishments, property seizures, or lien filings | No direct penalty for not filing, but collection actions proceed, and costs may increase. |

| Form 12153 — Request for a Collection Due Process (CDP) Hearing | Requests a formal due process hearing before levy or after lien notice | Must be filed within the strict deadlines stated on IRS notices | Disputing proposed levies or liens while seeking alternative payment arrangements | Missing the deadline forfeits CDP rights and allows enforced collection to continue |

| Form 9465 — Installment Agreement Request | Requests a monthly payment plan for tax debt | Filed when you cannot pay taxes in full immediately | Setting up structured payments to avoid aggressive collection | Failure to comply with the agreement can lead to default, renewed penalties, and collection actions |

| Form 433-A / 433-F — Collection Information Statement | Provides detailed financial information to determine the ability to pay | Required when applying for payment plans, hardship status, or Offers in Compromise | Demonstrating financial hardship or negotiating payment terms | Inaccurate or missing information can result in the denial of relief and continued enforcement |

| Form 656 — Offer in Compromise | Proposes settling tax debt for less than the full amount owed | Filed with full financial disclosure and application requirements | Resolving large tax debts when full payment is not feasible | Rejection leaves full liability in place; false information may trigger additional penalties |

By concentrating on promptly appealing an active collection action, Form 9423 stands out from the competition, as this comparison demonstrates. Choosing the correct form is critical, as using the wrong process can delay relief and allow enforcement measures to continue.

Comparison / Trade-off: DIY vs. Professional Help

Filing an appeal on your own costs less and gives you full control over your case, which may be suitable for straightforward issues with clear documentation. However, mistakes, incomplete information, missed deadlines, or misunderstanding IRS procedures can delay the process, weaken your argument, or even lead to the denial of the appeal.

Hiring a qualified tax professional involves higher upfront costs, but it can significantly improve accuracy and efficiency. Professionals understand how the IRS evaluates cases, what documentation carries the most weight, and how to present arguments in a way that aligns with IRS standards. They can also communicate directly with the agency on your behalf, reduce stress, and help prevent costly errors that could result in continued enforcement actions.

What Are the Step-by-Step Instructions for Filing IRS Form 9423?

Filing IRS Form 9423 properly ensures that taxpayers can effectively challenge IRS collection actions and protect their rights. Form 9423 consists of one page and has 17 data fields to complete, so accuracy is essential to avoid delays or penalties.

Step 1: Complete Basic Information – Fill in your personal details, including name, address, taxpayer identification number, and contact information. This ensures the IRS’s independent office can properly identify the case.

Step 2: Identify the Proposed Collection Action – Clearly indicate which IRS action you are appealing, such as a lien, levy, seizure, or rejected installment agreement request. Remember that the IRS will temporarily suspend collection actions after a taxpayer files Form 9423 until the appeal is resolved, unless the IRS believes collection is in jeopardy, in which case enforcement may continue.

Step 3: Explain the Dispute – Use the section labeled Reason for Appeal to outline your disagreement with the IRS decision. Taxpayers can propose a resolution to their disagreement with the IRS in Box 15 of Form 9423 to expedite a mutually acceptable outcome.

Step 4: Attach Supporting Documents – Include any evidence that supports your appeal, such as financial statements, correspondence with the IRS, or other relevant documentation. Following the form instructions carefully ensures your appeal is processed quickly.

Step 5: Sign and Date the Form – Your taxpayer signature is required for the appeal to be valid. Make sure Form 9423 is postmarked within three business days following a manager’s meeting, if applicable, to continue the appeal process.

Step 6: Submit the Form – Mail the completed form and attachments to the designated IRS office listed in the instructions, or follow online submission guidelines if available. After filing Form 9423, IRS collection actions will pause pending the resolution of the appeal, and the IRS aims to respond to collection appeal requests within five business days.

Step 7: Avoid Common Errors – Double-check that all 17 fields are complete, attachments are included, and deadlines are met. Missing information or late submissions can lead to unnecessary delays, penalties, or continued enforcement. Remember, the IRS will suspend enforcement action for the duration of an appeal regarding a proposed installment agreement, but only if the form is filed correctly.

Taxpayers can safeguard their rights and halt or halt IRS collection actions by adhering to the procedures and form instructions. Correct filing improves the likelihood of a speedy resolution to a tax dispute. By taking these steps, you can avoid needless fines or the worsening of a tax issue.

The C.L.E.A.R. Appeal Framework

- C – Clarify – Identify exactly what IRS action you are appealing.

- L – List Evidence – Gather all supporting documentation

- E – Explain – Provide factual, concise reasons for your appeal without emotional language.

- A – Ask for Resolution – State your desired outcome clearly.

- R – Review – Double-check deadlines, forms, and maintain a professional tone.

Gathering Required Documentation

Before completing Internal Revenue Service Form 9423, you should collect all documents that support your appeal or disagreement with the collection action. This typically includes a copy of the IRS notice you received, recent tax returns, proof of payments already made, bank statements, pay stubs, and any correspondence previously sent to or received from the IRS.

If your case involves financial hardship, you should also gather documentation of monthly expenses, assets, debts, and proof of income. Having complete and organized records helps ensure your appeal is processed without unnecessary delays.

Filling Out Personal and Tax Information

When filling out the form, you must carefully enter your full legal name, current address, Social Security Number or Employer Identification Number, and the tax periods involved. It is important to match this information exactly to IRS records, because even small discrepancies can slow processing or cause rejection.

You should clearly explain why you disagree with the collection action in the space provided, using concise and factual language supported by your documentation. A common mistake is leaving sections incomplete or providing vague explanations, which can weaken your appeal.

Submitting the Form and Follow-Up

After completing the form, you must submit it to the IRS employee listed on your notice or to the office handling your case, typically by fax or mail as instructed in the correspondence. You should keep copies of everything you send and, if mailing, consider using certified mail for proof of delivery.

Once submitted, the IRS will review your request, and you may be contacted for additional information or clarification. You can expect a written response outlining whether the collection action will be modified, suspended, or upheld, and you should respond promptly to any follow-up requests to avoid delays.

How Does IRS Form 9423 Fit Into IRS Compliance and Audit Processes?

IRS Form 9423 is an essential tool for taxpayers navigating IRS compliance and audits, as it allows them to formally challenge IRS collection actions while protecting their rights. The form is typically requested or required when the IRS is reviewing tax debt, proposed liens, levies, property seizures, or rejected installment agreement requests.

Filing the form correctly ensures that collection actions are paused, since the IRS will respond to all collection appeal requests within five business days. However, if the IRS believes collection is in jeopardy, it may continue collection actions despite a pending appeal.

Since inaccurate submissions can complicate audits, delay resolution, or result in additional IRS notices, the form must be filled out accurately. Also, Form 9423 interacts with other IRS procedures and notices. Taxpayers can halt enforcement, keep lines of communication open with the IRS, and improve the chances of a successful resolution of a tax dispute by completing the form as directed.

Common IRS Penalties Related to Form 9423

Failing to reply appropriately or promptly to Internal Revenue Service collection actions may result in further fines and financial repercussions. If necessary returns are not filed, taxpayers may be subject to late payment penalties, interest on outstanding balances, and enforced collection actions like liens or levies.

The IRS may uphold the initial collection action if incomplete, erroneous, or unsupported information is submitted with Form 9423, which could raise total expenses. You can reduce the risk of penalties by filing the form promptly after receiving the notice, ensuring all information is accurate, and attaching clear supporting documentation.

Keeping copies of submissions, following the instructions provided by the assigned IRS office, and responding quickly to any follow-up requests further helps prevent escalation. Timely communication demonstrates good-faith compliance, which the IRS considers during review.

If penalties have already been imposed, you may request that they be reduced, usually by providing a justification such as a serious illness, a natural disaster, or reliance on inaccurate professional advice. Typically, the abatement process entails requesting relief through an IRS representative or providing a written explanation accompanied by supporting documentation. Although approval is not assured, a successful abatement can lower the total amount owed by reducing or eliminating some penalties.

How Should You Respond to IRS Requests Involving Form 9423?

First, carefully review the IRS notice to identify the proposed collection action, deadlines, and any instructions provided. Second, complete Form 9423 accurately, following all form instructions, including providing a taxpayer signature and attaching any required supporting documents.

Third, submit the completed form promptly to the appropriate IRS office or as directed in the notice to ensure timely processing. Fourth, if the case is complex or involves significant tax debt, seek professional help from experts such as Victory Tax Lawyers.

Fifth, be prepared to provide more information upon request and monitor the response timeline, bearing in mind that the IRS will reply to all collection appeal requests within five business days. Taxpayers can safeguard their rights, halt enforcement actions, and effectively handle their tax issues by following these steps in order.

What Is the IRS Collection Appeals Program?

The IRS Collection Appeals Program (CAP) is a fast-track administrative process created by the Internal Revenue Service that allows taxpayers to challenge specific actions taken during the IRS collection process without going to court. Through an appeals review conducted by a collection manager or an independent appeals office, taxpayers may dispute enforcement measures such as a federal tax lien, levied property, or cases where the IRS rejects, modifies, or terminates an existing installment agreement.

The process typically begins after contact with an IRS revenue officer or local collection office and may lead to an appeals conference where the taxpayer can present their position and supporting documentation. CAP is significantly faster than a Collection Due Process (CDP) hearing, which often involves formal procedures and longer timelines.

Due to its speed, CAP can be critical when facing urgent enforcement actions such as wage garnishment, bank levies, or asset seizure, where immediate intervention may prevent serious financial harm. However, CAP only addresses how the IRS is collecting a tax debt. It does not allow you to dispute the amount owed.

Once a CAP determination is issued, it is final within the IRS administrative system, meaning neither the taxpayer nor the agency can request another administrative appeal on the same issue. Taxpayers who continue to experience hardship or believe the collection action creates an unfair financial burden may seek assistance from the Taxpayer Advocate Service, although this does not overturn the CAP decision itself.

Collection Appeals Program vs. Collection Due Process Hearing

There are two primary ways to challenge IRS collection actions. These are the Collection Appeals Program (CAP) and the Collection Due Process (CDP) hearing. Both processes are designed by the Internal Revenue Service to protect taxpayer appeal rights, but they serve different purposes and offer different levels of review. A CAP appeal focuses strictly on disputing how the IRS is collecting a tax debt, while a CDP hearing provides broader protections and legal rights.

A CAP appeal applies only to collection actions such as federal tax liens, levies, property seizures, or situations where the IRS rejects, modifies, or terminates an installment agreement. It does not allow you to challenge the amount of tax owed, penalties, or interest. In contrast, a CDP hearing allows you to dispute not only the collection action but also the underlying tax liability, penalties, and interest, making it the more comprehensive option when you believe the debt itself is incorrect.

You may qualify for a CAP appeal when the IRS files or proposes to file a tax lien, issues a levy notice, seizes or plans to seize property, or rejects or changes an installment agreement. This option is typically used when immediate action is needed to stop or modify enforcement measures. Because CAP cases move quickly, they can be especially useful when financial harm is imminent.

You qualify for a CDP hearing when the IRS sends a formal Notice of Intent to Levy or a Notice of Federal Tax Lien filing. These notices trigger specific legal appeal rights that allow you to request a hearing before enforcement proceeds further. To exercise these rights, you must submit Form 12153 within 30 days of the notice date.

If you miss the 30-day deadline, you generally lose the right to a full CDP hearing and the additional protections it provides. Although alternative options may still exist, they do not offer the same level of appeal rights or the ability to challenge the underlying tax debt. So, acting quickly is essential to maintain your strongest legal protections.

Pros and Cons of CAP and CDP

An important advantage of the Collection Appeals Program (CAP) is speed. You can resolve issues within a few days and stop IRS action. The process is also formal, so you may not have to attend a hearing. However, it also has its limitations. As stated earlier, CAP does not allow you to dispute the tax amount you owe. You can only file IRS Form 9423 to dispute a tax collection action. Also, once the IRS concludes CAP, you can not request further appeals within the agency.

When it comes to a Collection Due Process Hearing, you have full liberty to challenge both the collection action and the tax amount you owe. Plus, you maintain the right to escalate the issue to a tax court if you’re still unsatisfied and can request tax relief alternatives like an Offer in Compromise or penalty abatement. The disadvantage is that the speed of resolution is slower and may take several months. It also involves more paperwork and a formal process.

How Do You Write a Powerful Appeal Letter?

A powerful IRS appeal letter helps taxpayers communicate their intent clearly, include proper supporting documentation, and focus on resolving the issue efficiently. The goal is to help the IRS understand your position quickly and make a fair decision while preserving your right to appeal IRS collection actions.

Be Clear About What You’re Appealing

Start your letter by clearly describing the IRS collection action you disagree with, such as a lien, levy, seizure, or a rejected, modified, or terminated installment agreement. Include key details like the notice number, tax year, and date you received the notice. Remember, taxpayers have 30 days to appeal after their installment agreement has been rejected, modified, or terminated, so timing is critical.

Explain Your Reasons in Detail

When explaining why you disagree, stick to facts and avoid emotional language. If you experienced financial hardship, provide relevant details such as job loss, illness, or changes in income and expenses. A professional, respectful, and factual tone ensures the IRS evaluates your case based on evidence rather than emotion.

Include Supporting Documentation

Taxpayers must submit proof to support their appeal. Include copies of pay stubs, bank statements, medical bills, or any other relevant documents. Proper documentation strengthens your case and demonstrates credibility. Remember, taxpayers must file Form 9423 within 30 days of receiving the relevant IRS notice or within three business days of a conference with a Collection Manager.

Stay Respectful and Focused

Even if you believe the IRS acted unfairly, maintain a respectful and solution-focused tone. Avoid blaming or emotional appeals, as these do not help your case. Taxpayers need to notify the Collection office within two business days after a meeting with their manager to maintain proper communication and ensure compliance with IRS procedures.

Consider Working With a Tax Professional

If your case is complex or you are unsure how to clearly present your position, a qualified tax professional can help draft an accurate and compelling appeal letter. They understand how the IRS evaluates cases, what documentation is required, and how to avoid delays or rejection. For example, if the IRS does not respond to a request for a meeting with the collection manager within two business days, a professional can guide you on filing Form 9423 promptly to protect your appeal rights.

By following these steps, taxpayers can maximize their chances of a successful outcome when they appeal IRS collection actions, ensure deadlines are met, and properly communicate with the IRS Collection office and appeals system.

Real Example

A small business owner received a notice terminating her installment agreement due to unexpected medical bills. By submitting a detailed appeal with pay stubs, bank statements, and medical invoices, she successfully reinstated her payment plan within 25 days of receiving the notice. “A clear, well-documented appeal letter is often the difference between reinstating a payment plan and facing enforced collection,” says Amir Boroumand, managing attorney at VTL, with years of IRS negotiation experience.

Need a Tax Attorney for the Collection Appeals Process?

While a strong appeal letter significantly increases your chances, the IRS may still uphold collection actions if the evidence is insufficient. Preparing for alternative resolutions, like negotiating a payment plan or submitting an Offer in Compromise, is wise.

With over $72 million saved for clients since 2017, Victory Tax Lawyers, a Los Angeles-based tax firm, delivers experienced legal help you can count on to get real IRS solutions. Get the help you deserve. Contact us for a free consultation today!

Frequently Asked Questions

During the process of writing this blog, we encountered some frequently asked questions about Form 9423. We did our best to answer some of them.

What Is IRS Form 9423 Used For?

IRS Form 9423 is used to request a review of an IRS collection action through the Collection Appeals Program (CAP), such as a levy, lien, or seizure. It allows taxpayers to challenge how the Internal Revenue Service is collecting a tax debt without disputing the underlying amount owed.

Who Is Required to File IRS Form 9423?

No one is automatically required to file Form 9423; it is submitted voluntarily by taxpayers who disagree with a specific collection action. Individuals, businesses, or authorized representatives may file it when they want a fast administrative appeal of enforcement measures.

What Are the Deadlines for Submitting IRS Form 9423?

Deadlines are typically short and depend on the type of collection action, often requiring submission before or shortly after the action occurs. The exact timeframe is stated in the IRS notice or communicated by the assigned revenue officer, so prompt action is critical.

What Happens if IRS Form 9423 Is Filed Incorrectly?

If the form is incomplete, inaccurate, or lacks supporting documentation, the IRS may deny the appeal or proceed with the original collection action. Errors can also delay review, potentially allowing levies, garnishments, or seizures to continue.

Can I Respond to IRS Requests Related to Form 9423 Myself, or Should I Hire a Tax Attorney?

You may respond on your own if the situation is straightforward and you understand the issues involved. Hiring a qualified tax attorney or enrolled agent is advisable for complex cases, large liabilities, or when aggressive enforcement actions are underway.

Legal Disclaimer: The information provided on this blog is for general informational purposes only and does not constitute legal advice. Reading this content does not create an attorney-client relationship. Laws and regulations vary by jurisdiction and may change over time, so you should consult a qualified tax attorney for advice regarding your specific situation. Past examples, case studies, or hypothetical scenarios are illustrative only and do not guarantee similar results.

✓ Attorney-Reviewed Content

This content was written and reviewed by the licensed tax attorneys at Victory Tax Lawyers, LLP. Our attorneys specialize in IRS tax relief and are licensed members of the California State Bar with a nationwide practice.

Last Reviewed: 2026 · Meet Our Attorneys →