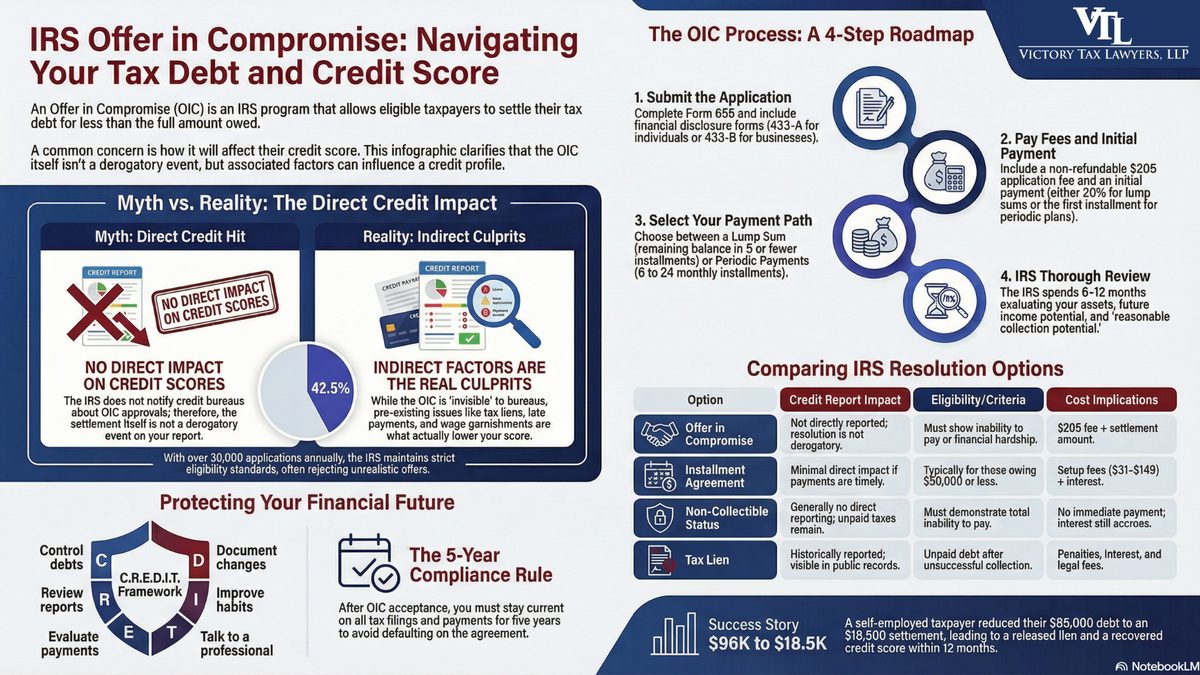

An Offer in Compromise (OIC) to settle for less than the full amount owed is a viable option for those experiencing difficulty in paying IRS taxes. An OIC itself is not reported to credit bureaus, so the approval does not directly lower your credit score. However, concerns regarding whether an OIC will harm your credit score or financial reputation persist. Making informed decisions and developing a strategic plan for financial recovery requires a thorough understanding of the credit ramifications.

At Victory Tax Lawyers, our seasoned tax professionals can help you prepare an Offer In Compromise. Schedule a free tax attorney consultation today.

This blog explains how an OIC affects credit and outlines strategies to safeguard and restore financial stability.

How Does an Offer in Compromise Appear on Your Credit Report?

An Offer in Compromise, also known as an IRS compromise, allows taxpayers to settle tax debt for less than the full amount owed when paying in full is not feasible. To apply, you must submit an IRS form with financial details about income, expenses, assets, and liabilities, thereby creating a structured path forward to resolve your tax obligations.

The approval itself typically does not appear on your credit report because the IRS does not notify the credit bureaus directly about an Offer in Compromise. However, your credit profile may be adversely affected by related actions that are already reflected in your credit history, such as tax liens, bank account levies, or collection actions like wage garnishment.

A key distinction exists between a tax lien and an OIC in credit reporting. While a tax lien may appear in public records and influence lenders’ decisions, an OIC is a resolution method rather than a reporting event. Once accepted, an OIC can function as a fresh start program, helping reduce tax debt and gradually improve your financial standing over time.

Common Myths about Offer in Compromise and Credit

Many taxpayers have misconceptions about how an Offer in Compromise (OIC) affects credit. One common myth is that an OIC always creates negative marks on your credit report, but in reality, the IRS does not report OIC approvals to credit bureaus. Another misunderstanding is that the IRS files information about your OIC based on your tax filing status or prior payments.

However, the only things that have a major effect on credit are preexisting conditions, like a federal tax lien, outstanding balances, or late payments. Your initial offer or whether you make a full payment through the IRS Program does not adversely affect your ability to secure a car loan or other forms of credit. By dismissing these misconceptions, taxpayers are better able to understand that an OIC is intended to offer tax relief without immediately affecting credit.

How Does an Offer in Compromise Affect Credit Scores and Overall Financial Health?

An Offer in Compromise does not directly lower your credit score because the IRS does not report OIC approvals to credit bureaus, but indirect factors connected to tax debt can still affect your credit profile. Previous tax liens, late payments, or collection actions may influence your score even before an OIC is approved, which means the impact often comes from the underlying tax issues rather than the settlement itself. After an OIC is accepted, many taxpayers begin to see gradual credit recovery as financial pressure is reduced and consistent payment behavior improves.

Financial institutions typically evaluate whether tax liabilities have been resolved, whether prior liens were released, how your payment history has changed, and whether your overall financial stability has improved since the OIC. These factors help lenders determine risk and long-term reliability, making an OIC not just a tax solution but a meaningful step toward stronger financial health.

Direct Credit Score Effects

An Offer in Compromise (OIC) is not directly reported to credit bureaus, so the resolution itself is not considered a derogatory event. Approval of an OIC does not automatically lower your credit score, making it a valuable tool for resolving tax debt without direct credit consequences. The key benefit is that it settles outstanding liabilities while avoiding negative notations tied to the compromise itself.

Indirect Factors Affecting Credit

Even though an OIC is not reported, prior tax issues such as a federal tax lien, late payments, or collection actions can still influence your credit. Tax liens may remain visible in public records up to seven years, and outstanding balances or missed payments before the OIC may temporarily negatively affect credit scores. Scenarios such as multiple prior liens, wage garnishments, or levies on bank accounts can continue to influence lender perceptions until fully resolved.

Credit Recovery Tips Post-OIC

After an OIC is accepted, rebuilding credit requires proactive steps, including monitoring your credit reports for accuracy and disputing any lingering errors. Paying existing bills on time, reducing overall debt, and maintaining consistent financial habits help restore creditworthiness over time. Using the OIC as a fresh start, taxpayers can gradually improve their scores while maintaining a positive financial record.

Real-Life Example: How an Offer in Compromise Improved a Taxpayer’s Credit Outlook

In one recent case we handled, a self-employed taxpayer owed over $96,000 in federal tax debt after several years of inconsistent income. Due to limited cash flow and rising living expenses, paying the full balance was unrealistic. After evaluating their financial situation, we helped them submit an Offer in Compromise of $18,500.

During the process, a federal tax lien had already affected their credit profile. Once the OIC was accepted and the lien released, their debt burden dropped significantly, and their credit score gradually improved over the next 12 months due to reduced financial stress and consistent payment behavior. This case demonstrates that while an OIC does not directly boost credit scores, it can create the financial stability needed for long-term credit recovery.

What Are the Alternatives to an Offer in Compromise and How Do They Affect Credit?

Taxpayers who cannot fully pay their IRS debt have several alternatives to an Offer in Compromise. This includes installment agreements, non-collectible status, and handling tax liens. An installment agreement allows taxpayers to pay off their debt over time, which generally has minimal direct impact on credit scores.

However, unpaid taxes before the agreement may have already affected the credit negatively. Non-collectible status temporarily suspends collection actions like wage garnishment or levies on bank accounts, and typically does not appear on credit reports. However, the IRS would monitor compliance closely in the future.

On the other hand, even though tax liens are no longer regularly reported by major credit bureaus, they can still have a significant impact on credit history, show up in public records, and influence lending decisions. There are trade-offs associated with each option. Tax liens indicate significant unpaid debt that may impair borrowing ability.

Non-collectible status offers instant relief but is only temporary, and installment agreements offer manageable payments but may incur interest. Knowing these differences will help taxpayers choose a plan that balances immediate financial relief with long-term credit health.

| Option | Description of Option | Credit Report Impact | Typical Duration of Credit Effect | IRS Eligibility Criteria | Cost Implications |

|---|---|---|---|---|---|

| Offer in Compromise (OIC) | Settles tax debt for less than the full amount owed | Not directly reported; the resolution itself is not derogatory | N/A for the OIC itself; prior liens or unpaid taxes may affect credit up to seven years | Must show inability to pay full tax liability, financial hardship, or doubt as to collectibility | Application fee ($205) and initial payment; total cost depends on settlement amount |

| Installment Agreement | Pay tax debt in monthly installments over time | Minimal impact if payments are made timely; prior unpaid taxes may affect credit | Prior liens may remain on report for seven years | Must owe $50,000 or less (for streamlined plans); other plans may require financial information and proof of ability to pay | May include setup fee ($31-$225) and penalties and interest on remaining balance |

| Non-Collectible Status (Currently Not Collectible) | Temporary suspension of collection actions due to financial hardship | Generally not directly reported; existing liens remain on record | Prior unpaid taxes may influence credit for up to seven years | Must demonstrate financial hardship and inability to pay any tax amount | No payment required while status is active; interest continues to accrue |

| Penalty Abatement | Legal relief against penalties for unpaid taxes due to reasonable cause | Penalties removed can positively influence credit; unresolved tax issues may still affect credit | Prior liens remain for seven years unless filing or release occurs | Must show reasonable cause; relief may be denied if unsuccessful | Reduces penalties, interest, and potential long-term negative credit impact once tax is settled |

Offer in Compromise vs Other IRS Solutions

While an Offer in Compromise can provide significant debt reduction, it is not always the best solution for every taxpayer. For example, taxpayers with stable income may benefit more from an installment agreement because approval is easier and long-term compliance may be simpler. Conversely, those facing severe financial hardship may find an OIC more effective despite the rigorous application process.

Each option involves trade-offs between cost, approval likelihood, and long-term credit impact. Evaluating these factors carefully helps taxpayers choose the most sustainable resolution strategy rather than pursuing an OIC solely because it appears more attractive.

What Is an IRS Offer in Compromise?

An IRS Offer in Compromise (OIC) is a program that allows taxpayers to settle their tax debts for less than the total amount owed. It is specifically designed to provide relief to individuals who are unable to fully pay their tax liabilities due to financial hardship. By aligning repayment terms with a taxpayer's unique financial situation, the program offers a manageable path to resolve overwhelming tax debt while restoring stability.

An IRS Offer in Compromise (OIC) is a program that allows taxpayers to settle their tax debts for less than the total amount owed. It is specifically designed to provide relief to individuals who are unable to fully pay their tax liabilities due to financial hardship. By aligning repayment terms with a taxpayer's unique financial situation, the program offers a manageable path to resolve overwhelming tax debt while restoring stability.

Each year, the IRS receives tens of thousands of Offer in Compromise applications. According to the IRS Data Book, more than 30,000 taxpayers submit OIC requests annually, but only about 40% to 45% are approved, reflecting the program’s strict eligibility requirements.

The OIC application process requires submitting Form 656 along with detailed financial documentation, including income, expenses, and asset information. The IRS carefully evaluates this data to determine if it meets eligibility criteria. Depending on their circumstances, not everyone can opt for a lump-sum offer or periodic monthly payments to meet their settlement obligations.

Are You Eligible for an IRS Offer in Compromise Program?

Eligibility for an OIC is not guaranteed, and only those demonstrating true financial hardship or liability disputes qualify. The process is highly selective, and the IRS uses stringent criteria to ensure the program is reserved for those in genuine need.

To qualify for an Offer in Compromise, taxpayers must first meet basic requirements, including filing all required tax returns and making current-year estimated tax payments. The IRS then evaluates each application based on three primary grounds.

The first ground is doubt as to liability, which applies when there is a legitimate question about whether the tax amount assessed by the IRS is accurate. For example, a taxpayer who disputes an IRS assessment due to clerical or calculation errors may qualify under this criterion.

The second ground is doubt as to collectability, which arises when a taxpayer’s financial situation shows that they cannot reasonably pay the full tax debt within the statutory collection period. For instance, a taxpayer with limited income and substantial medical expenses may fall into this category.

The third ground is effective tax administration, which applies when paying the full tax debt would create undue financial hardship, even if the IRS could technically collect the amount owed. For example, a retired taxpayer who relies solely on Social Security income may qualify under this basis.

Maintaining estimated tax payments is a critical component of eligibility. Doing so helps keep the taxpayer compliant with IRS requirements throughout the application process. Falling behind on these payments could jeopardize your application and payment options, so careful planning and ongoing diligence are essential for passing IRS reviews.

According to experienced tax attorneys, the most common reason OIC applications fail is unrealistic offers that do not align with the taxpayer’s true financial capacity. “In our experience, the strongest Offer in Compromise applications are those supported by accurate financial documentation and realistic settlement proposals,” explains Parham Khorsandi, an experienced tax attorney at Victory Tax Lawyers. “When done correctly, an OIC can reduce tax debt while preserving long-term financial stability.”

How Does an Offer in Compromise Work?

Navigating the IRS's Offer in Compromise pathway requires a meticulous approach. The process is detailed and involves several steps, from application to IRS decision:

Step 1. Submit the OIC Application

The first step is gathering all the relevant documentation that serves as evidence of your financial situation. Start by downloading the Form 656-B Booklet, which basically outlines every form you need to complete and submit your OIC application. This includes Form 433-A for wage earners or self-employed individuals, or Form 433-B for business operators.

Both forms detail your financial information. There is also Form 656. This is your official offer to the IRS. Here, you'll outline the tax years and the specific tax you are requesting a compromise for. You will need to submit separate forms if you are resolving both personal and business tax debts. The financial details provided on this form must be accurate and comprehensive.

Step 2. Pay the Application Fee and Initial Payment

Submitting an OIC comes with upfront non-refundable costs. The application fee is $205, and as we mentioned, it is non-refundable even if your offer ends up being rejected. In addition to your application fee, you'll need to include an initial payment for each Form 656 you submit.

The initial payment is also non-refundable. However, it will be applied to reduce your tax debt if your offer ends up being approved. These fees demonstrate your commitment to resolving your tax debt and are part of the offer submission process.

Step 3. Make Payment

You have two payment options to choose from for your initial payment: periodic payment or lump sum cash payment. If you'd rather make payments periodically, you'll be required to submit your first installment with your application and continue to make monthly payments while the IRS reviews your offer. If your offer is accepted, you will continue to make monthly payments over a stipulated period, typically within 6 to 24 months.

The IRS requires that your application fee include 20% of the entire offer amount if you choose the lump sum cash payment plan. If your offer is approved, you are then to pay up the remaining balance in no more than five installments.

When considering the payment plan for settlement, make a judicious choice based on your financial capacity. A lump-sum payment can signal to the IRS your urgency and capability to resolve your remaining balance and tax issues swiftly. By paying 20% upfront, you not only reduce the total amount owed but also potentially speed up the acceptance process by demonstrating immediate financial commitment.

On the other hand, periodic payments allow for breathing room, spreading your tax burden over up to 24 monthly installments. It's tailored for those who need time to reorganize their finances while still showing commitment to settling their IRS debt.

Step 4. Wait for IRS Review

The IRS checks your assets against your outstanding tax liability. A financial lifeline is provided by an Offer in Compromise, but there are important factors to consider. Usually, the review period spans anywhere from six to twelve months. The IRS's scrutiny in the Offer in Compromise process is quite thorough.

They consider multiple factors when evaluating your offer, including all the documents you must have provided, such as your bank statements and tax returns. They also check your financial statements over the past two years.

Beyond numbers, they look at your financial habits, future income potential, and whether the offer aligns with your long-term financial stability. Their analysis involves evaluating your employment status, potential for income growth, and any debts, living expenses, or liabilities that could affect your financial future.

In addition to these, they assess your asset equity to determine if liquidating assets like real estate or stocks could cover your tax debt. Finally, the IRS checks your overall financial health and your ability to pay. All of these are done to confirm that your offer genuinely reflects your assertion of being unable to pay your full tax debt.

Pros and Cons of an Offer in Compromise on Your Financial Health

An Offer in Compromise can serve as a financial lifeline; however, it is accompanied by important considerations. Taxpayers can make well-informed decisions that support their financial objectives by being aware of both the benefits and the drawbacks. The table below outlines the key pros and cons to consider.

| Pros | Cons |

|---|---|

|

|

When compared to other tax resolution methods like installment agreements or partial payment plans, an OIC might offer quicker relief but requires a significant upfront commitment in terms of documentation and an initial payment option that is non-refundable.

How Can You Minimize Credit Impact While Pursuing an Offer in Compromise?

Strategic foresight is essential when dealing with tax debt, especially if you wish to minimize the credit impact while pursuing an Offer in Compromise (OIC). One effective approach is to manage your credit meticulously by ensuring timely payments on all other debts and maintaining low credit utilization. The IRS will evaluate your reasonable collection potential and your ability to meet required payments during the OIC review process.

It is also important to avoid tax liens whenever possible or address existing liens promptly by negotiating a lien release and resolving outstanding tax liabilities through payment or settlement. Maintaining good credit-building habits is equally critical, which includes regularly reviewing your credit report for errors, practicing responsible financial management, and minimizing monthly expenses while the IRS determines your eligibility for a compromise.

Finally, seeking professional guidance from an experienced IRS tax attorney can greatly improve your chances of success. They can assist you in navigating the complexities of the Offer In Compromise application and work to secure the best possible outcome while safeguarding your financial future and minimizing potential negative effects on your credit.

The CREDIT Framework: A Practical Method to Protect Your Credit During an OIC

To help taxpayers protect their credit while pursuing an Offer in Compromise, we use the C.R.E.D.I.T. framework:

- C — Control outstanding debts: Stay current on non-tax obligations to prevent additional negative marks.

- R — Review credit reports regularly: Identify and dispute errors tied to tax liens or collections.

- E — Evaluate payment options carefully: Choose an OIC payment structure that fits your financial reality.

- D — Document financial changes: Keep records of income shifts or unexpected expenses to communicate with the IRS.

- I — Improve financial habits: Reduce credit utilization and build a consistent payment history.

- T — Talk to a tax professional early: Strategic guidance can prevent costly mistakes and credit damage.

This structured approach helps taxpayers reduce risk while maximizing the benefits of an OIC.

What Happens After the IRS Accepts Your Offer In Compromise?

When the IRS accepts your Offer in Compromise (OIC), it is an important milestone, but it does not mark the end of your responsibilities. The work continues because any default on your part can undo the agreement and place you back in the same position as before. So, it is essential to follow all conditions of the settlement carefully.

You must stay current on all required payments and choose a payment plan that realistically fits your financial situation. If you selected periodic payments, you must consistently set aside a portion of your income to meet your monthly obligations until the debt is fully paid. If you agreed to a lump-sum payment arrangement, you need to manage your budget carefully to ensure you meet the terms of the agreement without exceeding deadlines.

Maintaining tax compliance is also important after your offer is approved, as the IRS requires you to file all tax returns on time and pay taxes promptly for at least five years following the acceptance of your OIC. In addition, you should maintain open communication with the IRS. If your financial circumstances change, if you miss a payment, or if you make an error on a tax return, you must notify them. Addressing issues early can help you avoid default and preserve the benefits of your settlement.

What Happens to My Credit if My OIC Is Rejected?

An OIC rejection does not directly affect your credit score. However, unresolved tax debts might lead to liens and impact your financial credibility and acceptance rate. A rejected OIC can strain your financial stability, as you'll need to find another way to deal with your tax debt, potentially delaying credit recovery. If the IRS rejects your OIC, explore other IRS payment plans or appeal the decision.

Need a Tax Professional for Your Offer in Compromise?

Unlike generic explanations of the Offer in Compromise process, this guide focuses on the real-world credit implications of tax debt resolution. By combining legal insights, financial strategies, and practical credit-rebuilding guidance, it provides a comprehensive roadmap for taxpayers who want to resolve IRS debt without jeopardizing their financial future. Our approach is grounded in real client experience, strategic frameworks, and actionable steps that go beyond what the IRS expects, making this resource a practical tool rather than a theoretical overview.

With over $100 million saved for clients since 2017, Victory Tax Lawyers, a Los Angeles-based tax firm, delivers experienced legal help you can count on to get real IRS solutions. Get the help you deserve. Contact us for a free consultation today!

Frequently Asked Questions

During the process of writing this blog, we encountered some frequently asked questions related to the IRS Offer in Compromise. We did our best to answer some of them.

Does an Offer in Compromise Show Up on My Credit Report?

An Offer in Compromise (OIC) itself is not reported to credit bureaus, so approval does not directly appear on your credit report. However, any prior tax liens or unpaid taxes may already be listed and could influence your credit history.

How Long Does an Offer in Compromise Affect My Credit?

Since the OIC itself is not reported, it does not have a direct credit duration. Indirect effects from federal tax liens or late payments may linger up to seven years on credit reports.

Can an Offer in Compromise Remove a Tax Lien From My Credit Report?

An OIC can result in the IRS releasing a federal tax lien if the debt is settled, which may improve how lenders view your credit. Once the lien is released, any credit report impact related to that lien is typically updated, though public records may still show historical filings.

What Are the Credit Differences Between an Offer in Compromise and an Installment Agreement?

An OIC settles your tax debt for less than the full amount and is generally not reported to credit bureaus, while installment agreements may not directly appear, but unpaid balances before the plan could negatively affect your credit. Choosing an OIC versus an installment plan through an IRS Program can offer a faster resolution and clearer path to rebuilding credit.

How Can I Improve My Credit Score After Settling Tax Debt With an OIC?

Monitor your credit reports carefully and dispute any inaccuracies related to prior tax liens or debts. Consistently paying bills on time, reducing debt, and maintaining responsible financial habits will gradually restore your credit score after an OIC.

Legal Disclaimer: This content is provided for informational purposes only and does not constitute legal or tax advice. Reading this article does not create an attorney-client relationship. Tax situations vary, and you should consult a qualified tax attorney or tax professional regarding your specific circumstances before taking action.