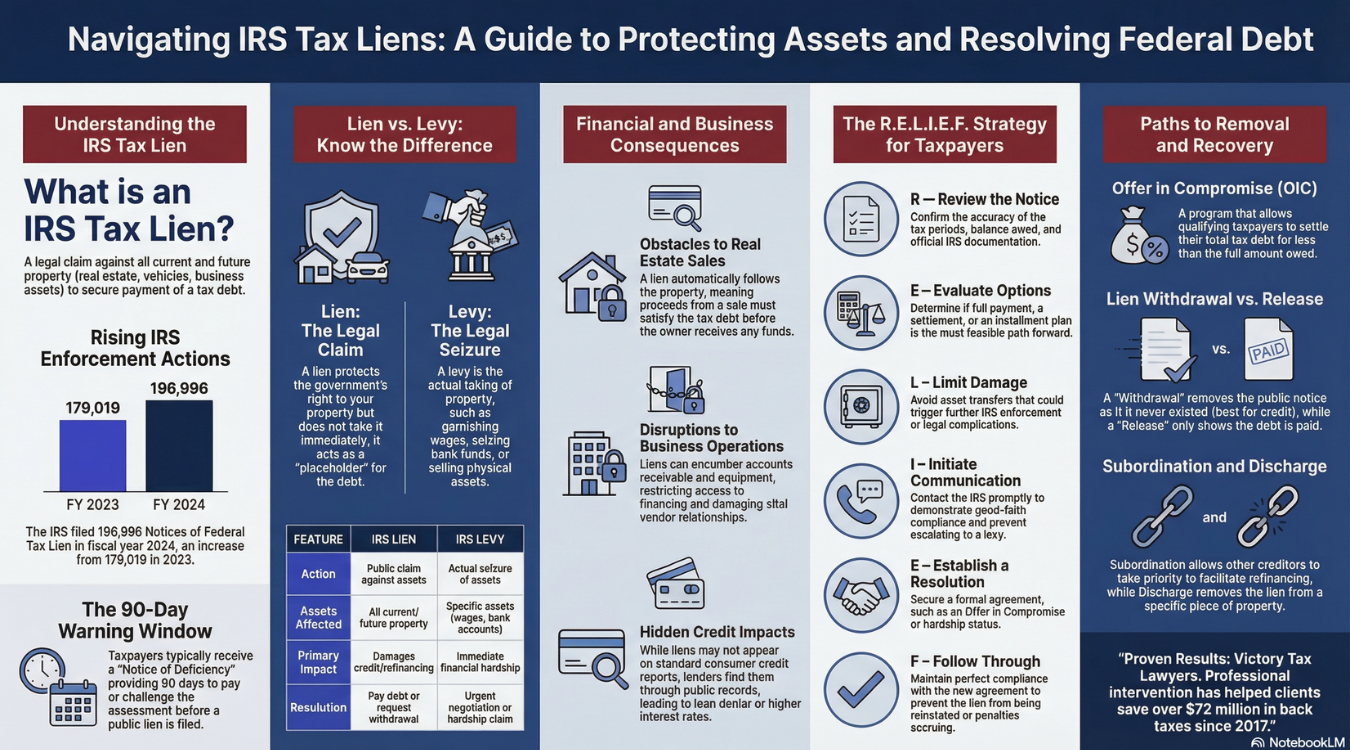

An IRS tax lien, or federal lien, is a legal claim the government places on a taxpayer’s property when they neglect or fail to pay their tax debt. A lien secures and protects the government’s interest in all your assets, including real estate, bank accounts, and even future earnings, until the debt is resolved. If you’re at risk of failing to pay your business taxes, it is important to understand that tax liens can negatively impact you and your business. In extreme cases, ignoring an IRS tax lien can have even more severe consequences as it counts as debt neglect and, if suspected, can result in seizing your assets for sale.

At Victory Tax Lawyers, our seasoned tax professionals can help with tax liens. Schedule a free tax attorney consultation today.

This post will explain what a tax lien is, how it affects you, and the difference between a tax lien and a tax levy.

What Is an IRS Lien and How Does It Work?

An IRS lien or a federal tax lien is the government’s legal claim against your property when you fail to pay a tax debt. Whether a federal tax lien is due for payroll taxes, income taxes, or even estate taxes, the Internal Revenue Service acquires a secured interest in your debtor’s assets to guarantee that the money is eventually collected.

Once the tax is assessed, a demand for payment is sent, and if the remaining amount is not paid, the lien is created. In order to defend its rights at this stage, it may file a public notice. Though the IRS may occasionally withdraw or release the lien if doing so serves the government’s best interest and improves the likelihood of recovery, the claim usually remains in effect until the debt is fully paid or the applicable collection statute expiration date passes.

This claim is very broad because it applies to almost all of your current and future property. This includes real estate such as the taxpayer’s home, cars, and other personal belongings, bank accounts and other financial assets, business interests, and even revenue streams such as accounts receivable. This means that almost anything of value associated with the taxpayer can be encumbered while the lien is in place. It’s critical to understand the difference between a lien and a levy.

A lien is simply a legal claim that protects the government’s interest, while a levy is the actual taking of property, such as taking money out of accounts or garnishing wages. While taxpayers may contest IRS actions in tax court or through administrative channels, there are strict deadlines.

A federal tax lien can significantly disrupt financial life because lenders frequently discover it through public records, even when it does not appear on standard credit reports. This can make borrowing, refinancing, or transferring ownership difficult. Moreover, when property is sold, the lien typically must be satisfied from the proceeds before the owner receives any remaining funds. However, the IRS does agree in some situations to subordinate or discharge the lien to allow a sale or refinancing to proceed if it enhances the government’s likelihood of successful collection.

What Are the Consequences of an IRS Lien on Your Finances and Credit?

When a federal tax lien exists, it signals that serious tax liability and unpaid taxes remain outstanding. Furthermore, once a tax lien is filed, the government gains a legal claim over the debtor’s property to secure payment under authority granted by the Internal Revenue Code.

Although federal tax liens no longer appear on most standard credit reports, lenders, landlords, and financial institutions often discover them through public records. This can still lower borrowing power, trigger loan denials, increase interest rates, or prevent approval for mortgages, credit lines, or leases.

A lien can also create major obstacles when trying to sell or refinance real estate because the claim automatically follows the property. This means proceeds from any sale must be used to satisfy the debt before the owner receives funds, and refinancing may be blocked unless the Internal Revenue Service approves the transaction.

According to the Internal Revenue Service Data Book, the IRS filed 179,019 Notices of Federal Tax Lien in fiscal year 2023 and 196,996 in fiscal year 2024, reflecting continuing use of liens as an enforcement tool. In certain circumstances, the IRS agrees to subordinate or discharge its claim if doing so improves the chances of collection.

For business owners, the impact can be severe because a lien on business property can disrupt operations, restrict access to financing, damage vendor relationships, and place claims on revenue streams. Thereby making it difficult to maintain normal cash flow or obtain supplies on credit.

In all cases, the lien remains in effect until the tax debt is paid, settled, withdrawn, or legally discharged. This means the government retains its claim over your debtor’s property for years while interest and penalties may continue increase.

How Does a Federal Tax Lien Affect Business and Personal Property?

When a federal tax lien is filed by the Internal Revenue Service, it attaches to all current and future property you own, including both business and personal assets. This means the government gains a legal claim over those assets until the tax debt is fully resolved or the lien expires.

For businesses, the lien can encumber critical operating assets such as equipment, inventory, accounts receivable, and real estate. This can restrict the company’s ability to obtain financing, sell assets, or attract investors, since lenders and buyers typically require a clear title before proceeding. In severe cases, the lien can disrupt daily operations if cash flow options become limited.

Personal property is also at risk. The lien can attach to your home, vehicles, bank accounts, and other valuable assets, even if they are not directly related to a business. Additionally, the presence of a public lien filing can damage creditworthiness, making it harder to qualify for loans, credit cards, or favorable interest rates.

Common practical consequences include:

- Property sales complications: You may be unable to sell real estate or other major assets unless the lien is paid, released, or formally subordinated at closing.

- Refinancing difficulties: Mortgage lenders often refuse refinancing requests while a lien is active because the IRS claim takes priority.

- Credit approval delays or denials: Financial institutions may view the lien as a significant risk, slowing approvals or resulting in outright rejection.

- Business financing barriers: Lines of credit, equipment loans, and investor funding may be restricted due to the government’s secured interest.

- Encumbrance of future assets: Property acquired after the lien filing can also become subject to the lien until the debt is resolved.

Since these impacts can escalate quickly, taxpayers facing a lien should consider prompt action, such as payment arrangements, negotiation with the IRS, or professional tax representation, to protect both business continuity and personal financial stability.

What Should You Do When the IRS Places a Lien on You?

First, verify that the lien is valid by reviewing the official notice, confirming the tax amount owed, the tax periods involved, and ensuring the debt actually belongs to you. If errors exist, contact the IRS immediately and submit documentation to dispute or correct the record.

Next, explore resolution options such as paying the balance in full, setting up an installment agreement or payment plan, or applying for an Offer in Compromise if you cannot afford to pay the total amount. Taking action quickly can prevent additional penalties, interest, or enforcement measures.

If a natural disaster, a serious illness, or other uncontrollable circumstances prevented you from filing or paying on time, you may also request a penalty abatement. This can lower the overall debt and make the settlement easier to handle.

It is strongly advised to seek assistance from a qualified tax attorney, certified public accountant, or enrolled agent due to the significant financial and legal ramifications of a tax lien. Having legal counsel can guarantee that your rights are upheld, that negotiations are conducted appropriately, and that the lien is settled as quickly as possible.

When and How Can You Request Withdrawal of an IRS Lien?

You may request the withdrawal of a federal tax lien when specific conditions set by the Internal Revenue Service are met. Common situations include paying the tax debt in full, entering into a qualifying direct-debit installment agreement, filing the lien in error, or demonstrating that withdrawal will facilitate collection. In some cases, taxpayers who owe below certain thresholds and maintain timely payments may also qualify.

The request is made using IRS Form 12277. You must complete the form with your identifying information, details about the lien, and the reason you believe withdrawal is appropriate, then submit it to the IRS office that filed the lien. Supporting documentation can strengthen the request. The IRS will review the application and notify you of approval or denial.

The advantages of a lien withdrawal are greater than those of a typical lien release. By removing the public notice as if the lien had never been filed, a withdrawal can greatly increase creditworthiness and lessen barriers when selling or financing real estate. Whereas a release only signifies that the debt has been paid off and the lien is no longer enforceable. Due to this distinction, withdrawals are especially beneficial for taxpayers who want to improve their financial situation after paying their taxes.

Real Client Scenario: How a Business Owner Removed a Tax Lien Without Closing Operations

In a recent case we handled, a restaurant owner in Los Angeles accumulated over $185,000 in unpaid payroll taxes after revenue dropped during a prolonged downturn. The IRS filed a Notice of Federal Tax Lien, preventing refinancing and threatening vendor relationships.

Working with our experienced tax counsel, the owner entered a direct-debit installment agreement and demonstrated that removing the public lien would improve the government’s ability to collect. The IRS approved a lien withdrawal after six months of consistent payments, allowing the business to secure financing and remain operational. Cases like this show that a lien does not automatically mean financial collapse, but ignoring it can quickly escalate enforcement actions.

What Is the Difference Between an IRS Lien and an IRS Levy?

An IRS lien is a legal claim against your property, while an IRS levy is the actual seizure of your property to satisfy a tax debt. When the Internal Revenue Service files a lien, it secures its interest in your assets, such as your home, car, or financial accounts, but does not take them immediately.

A levy, by contrast, allows the IRS to take property or funds directly, such as garnishing wages, withdrawing money from bank accounts, seizing rental income, or even taking and selling physical assets. In simple terms, a lien protects the government’s right to your property, while a levy exercises that right.

Levies can affect ongoing income sources, including paychecks and Social Security benefits, making them more immediately disruptive than liens. Because of this, the IRS typically issues advance notices and provides an opportunity to resolve the debt before a levy begins.

Taxpayers can request a lien withdrawal or subordination, pay the debt, establish a payment plan, or contest the liability if it is incorrect to stop or contest a lien. Urgent measures, such as signing an installment agreement, demonstrating financial hardship, submitting an appeal, or negotiating the levy’s release with a tax expert, are typically necessary to halt a levy.

IRS Lien vs. IRS Levy: What’s the Difference?

| Feature | IRS Lien | IRS Levy |

|---|---|---|

| Definition | A legal claim against your property to secure payment of a tax debt | The legal seizure of property or assets to pay the tax debt |

| What it affects | All current and future property, including real estate, vehicles, business assets, and financial accounts | Specific assets such as wages, bank accounts, Social Security benefits, rental income, or physical property |

| How it is enforced | Filed as a public notice (Notice of Federal Tax Lien) establishing the government’s priority over other creditors | Executed through direct action, such as wage garnishment, bank account levy, or asset seizure and sale |

| Impact on the taxpayer | Damages creditworthiness, restricts the ability to sell or refinance property, and complicates borrowing. | Immediate financial hardship due to loss of income or funds can disrupt daily living or business operations. |

| How to resolve | Pay in full, enter an installment agreement, request lien withdrawal/subordination, or dispute the liability | Urgent action required: pay the debt, set up a payment plan, prove financial hardship, file an appeal, or negotiate release |

It is essential to comprehend this difference; a levy exercises the government’s right to seize assets, whereas a lien safeguards that right. Early action can minimize financial harm and maintain your options for paying off the tax debt before a lien turns into a levy.

When Does the IRS File a Tax Lien?

The IRS does not file a tax lien without warning. You will first receive a notice stating that you owe unpaid federal taxes. This notice explains the amount due and how to pay. A lien is not the IRS’s first action when a taxpayer fails to meet their tax obligations. You are given time to respond. You can pay the debt or dispute the amount. Ignoring the notice can lead to stronger collection actions. Removing a lien later can be slow and difficult.

Your best response is to act quickly. Pay the balance in full if possible. If you believe the notice is incorrect, contact the IRS to verify the information. You may also need to file a missing tax return if one was not submitted. Delay can increase penalties and interest. The process usually begins with a Notice of Deficiency. This letter is often called a 90-day letter because it gives you 90 days to respond or challenge the assessment. If you do nothing during this period, the IRS may move forward with collection.

After the deadline passes, the IRS may file a Notice of Federal Tax Lien. This filing becomes a public record. It alerts creditors that the government has a legal claim to your property. Filing the lien also gives the IRS priority over other creditors.

Tax liens are commonly filed when the debt is $10,000 or more. However, smaller debts can still result in a lien if collection appears at risk. In some cases, a lien can be filed soon after final notice. Early communication with the IRS can often prevent this step.

How Do You Know If You Have an IRS Tax Lien?

If you’re unsure if a tax lien has been filed against you, here are some steps you could take to find out:

- Contact the IRS Centralized Lien Unit: The first way to confirm whether or not you have a tax lien is to call the IRS Centralized Lien Unit at 800-913-6050 or e-fax 855-390-3530. They can provide direct confirmation and details regarding any lien placed against you. If no lien has been filed yet but you suspect one may be filed soon, immediately log into your IRS account, check your current balance, and pay it off to prevent further IRS action.

- Look for an IRS Notice of Federal Tax Lien (NFTL): The IRS sends a formal notice when they place a lien on your assets. If you owe back taxes and a lien has been filed, you would have received this notice by mail. So, carefully check your IRS correspondence to confirm the receipt of the notice.

- Review Your Tax Records: If you prefer to verify the lien status yourself, log into your IRS online account and check for outstanding tax debts. You can also request a transcript of your tax account (online or by mail). It will show any current liens. If you see a balance due, immediately clear it up so that the IRS doesn’t file a lien against you.

- Check Public Records: The IRS files tax liens with local government offices, usually at the county or state level. You can search your county recorder’s office or the secretary of state’s website to see if a lien has been placed against you. Some legal databases also provide lien status information for a fee.

- Monitor Your Credit Report: While tax liens no longer appear on consumer credit reports, financial institutions can still access lien information in some cases. If you tried securing a loan or refinancing and were denied, this may be a sign that a tax lien is affecting your financial standing. A lien won’t affect your credit score, but since it’s public information, it may affect lenders’ perceptions of your creditworthiness, which in turn could affect your ability to obtain credit.

- State & Local Tax Liens: The IRS isn’t the only agency that can file a lien. State and local governments can also place liens on your property for unpaid state taxes. If you suspect a state tax lien, check with your county office or state tax authority. For example, in California, taxpayers can set up a payment plan for a $34 fee, allowing them to gradually clear their state tax debt. Once the liability is paid off, the lien can be removed.

- Watch for Legal or Financial Restrictions: A tax lien can make it difficult to sell property. If you’re denied credit or refinancing, you need to check to see if a lien is the cause.

What Should You Do If You Receive an IRS Tax Lien Notice?

Receiving an IRS tax lien notice is a serious matter that requires immediate attention. The first thing you want to do is review the notice carefully to confirm the accuracy of all information contained in the notice. Compare the information with your tax record, and if you find any discrepancy, carefully follow the instructions in the notice and meet all response deadlines to avoid further complications.

If the lien is valid and you owe back taxes, it is best to take action to remove the lien by paying your debt in full. If you’re unable to fully pay your tax bill, perhaps due to financial hardship, the IRS provides other tax relief options, such as an installment agreement, penalty abatement, or Offer in Compromise, that may be available to you.

Always consult a tax professional when dealing with IRS issues, especially if you’re facing a tax lien. A tax professional can help you determine the best course of action based on your financial situation. If such needs arise, a tax attorney knows how to effectively negotiate with the IRS on your behalf.

The R.E.L.I.E.F. Strategy for Handling an IRS Tax Lien

Taxpayers facing a lien can follow the R.E.L.I.E.F. framework to reduce risk and regain financial stability:

- R — Review the Notice: Confirm accuracy, tax periods, and balance owed

- E — Evaluate Options: Determine whether full payment, installment agreement, or settlement is feasible

- L — Limit Damage: Avoid asset transfers or actions that could trigger further enforcement

- I — Initiate Communication: Contact the IRS promptly to demonstrate good-faith compliance

- E — Establish a Resolution: Secure a payment plan, Offer in Compromise, or hardship status

- F — Follow Through: Maintain compliance to prevent levy or additional penalties

This structured approach helps prevent panic-driven decisions and ensures critical deadlines are not missed.

How to Remove an IRS Tax Lien

A lien isn’t a death sentence. There are several ways to remove an IRS tax lien:

1. Paying the Tax Debt in Full

The most effective way to get rid of a federal tax lien is to pay your tax debt in full. Once the IRS receives your full payment, they’ll release the lien within 30 days. The IRS will further update the public that the lien has been lifted.

2. Setting Up a Payment Plan

If you’re unable to pay your tax debt in full, you could request an IRS installment agreement. Setting up payment plans allows taxpayers to pay their back taxes over time in manageable monthly payments, thereby lessening the stress on their finances. However, interest and penalties still accrue on the unpaid balance.

3. Offer in Compromise

An offer in compromise (OIC) is another popular tax relief option for taxpayers struggling to pay their IRS debt in full. An OIC lets you pay less than you owe, although you’ll have to meet certain stringent criteria to qualify for this program. The IRS can also deny your offer if it doesn’t find your claim convincing enough; hence, it’s advisable to work with a tax lawyer if you’re considering using this option.

4. Discharge of Property

Taxpayers can also apply for a certificate of discharge. A discharge of property removes a lien from specific properties you own. In a case where you want to sell the property, a discharge of property makes it easier to find buyers. Otherwise, the IRS will have the upper hand, discouraging interested buyers.

5. Subordination

Consider applying for a certificate of subordination, which allows creditors to take priority over the IRS, making it easier for you to sell your assets. Subordination doesn’t apply to all assets, however. You must also meet certain eligibility requirements by the IRS when applying for subordination. Note that lien subordination does not remove your tax lien or your legal obligation to pay; it only allows other creditors to get priority treatment.

Comparison / Trade-Off Analysis: Handling a Tax Lien Yourself vs. Hiring Professional Help

Resolving a lien independently may save money initially and can be appropriate for smaller debts with straightforward circumstances. However, taxpayers must navigate complex IRS procedures, strict deadlines, and negotiation requirements on their own. Mistakes can prolong the lien or lead to harsher enforcement.

Professional representation involves upfront costs but often results in faster resolution, stronger negotiation outcomes, and reduced risk of errors. Attorneys and enrolled agents understand which relief programs are most viable and how to present financial information effectively.

Need Legal Help with Your IRS Tax Lien?

In our experience assisting taxpayers with complex IRS matters, many individuals delay action out of fear or confusion, which often allows penalties and enforcement risks to grow unnecessarily. As against popular belief, a tax lien doesn’t mean that the IRS has seized your property to satisfy your debt. Instead, it’s a claim against your assets. And the earlier you respond to the IRS’s notice, the better your chances of arriving at a safer outcome regarding settling your back taxes.

With over $72 million saved for clients since 2017, Victory Tax Lawyers, a Los Angeles-based tax firm, delivers experienced legal help you can count on to get real IRS solutions. Get the help you deserve. Contact us for a free consultation today!

Frequently Asked Questions

During the process of writing this blog, we encountered some frequently asked questions related to IRS tax liens. We did our best to answer some of them.

What Does an IRS Lien Mean for My Credit?

An IRS lien signals to lenders that the Internal Revenue Service has a legal claim on your property due to unpaid taxes. Even though federal tax liens no longer appear on most consumer credit reports, lenders can still discover them through public records and may deny credit or offer worse terms. While liens can create serious obstacles, many taxpayers successfully resolve them through payment plans or negotiated settlements, and the impact often improves once the debt is addressed.

Can the IRS Take My Home With a Lien?

A lien alone does not mean the IRS will take your home. However, it gives the government a legal claim, and the property could be seized later through a levy if the debt remains unresolved.

How Long Does an IRS Lien Stay on My Record?

An IRS lien generally remains in effect until the tax debt is paid in full or becomes legally unenforceable. This period is usually up to 10 years from the date the tax was assessed, though certain actions can extend it.

How Do I Remove an IRS Lien?

You can remove a lien by paying the debt in full, setting up a qualifying payment plan, or obtaining a withdrawal after meeting IRS requirements. In some cases, discharge, subordination, or successful dispute of the liability can also eliminate or lessen the lien’s impact.

What Is the Difference Between an IRS Lien and Levy?

A lien is a legal claim against your property to secure payment of unpaid taxes. A levy is the actual seizure of wages, bank funds, or assets to satisfy the tax debt.

✓ Attorney-Reviewed Content

This content was written and reviewed by the licensed tax attorneys at Victory Tax Lawyers, LLP. Our attorneys specialize in IRS tax relief and are licensed members of the California State Bar with a nationwide practice.

Last Reviewed: 2026 · Meet Our Attorneys →